On July 17, 2019, the Internal Revenue Service (IRS) released Notice 2019-45, which expands the definition of preventive care benefits that can be provided by a high deductible health plan (HDHP) to include certain chronic conditions. The guidance in the Notice may be relied upon immediately. In general, most HDHP participants may establish and contribute to a health savings account (HSA), unless there is disqualifying coverage—such as having other medical benefits available besides preventive care before the minimum annual deductible is satisfied.

Overview

Under Section 223(c) of the Internal Revenue Code (Code), an HSA-qualified HDHP is not required to impose a deductible for certain preventive care services. This preventive care safe harbor includes services such as annual physicals, well-childcare, and immunizations. Notably, prior to the Notice, preventive care did not include any service to treat existing illnesses, injuries, or conditions. Likewise, drugs or medications were treated as preventive care only when taken by a person who has developed risk factors for a disease that has not yet manifested itself or has not yet become clinically apparent (i.e., the individual is asymptomatic) or when the drugs are taken to prevent the recurrence of a disease from which a person has recovered.

Ultimately, the goal of the preventive care safe harbor is to encourage HDHP participants to receive routine care with a lower cost barrier, which should lead to better health outcomes. By expanding the list of medical services that can be classified as preventive care, the IRS recognizes that cost barriers for care have resulted in some individuals with certain chronic conditions failing to seek care that would prevent exacerbation of their condition, which can lead to consequences such as amputation, blindness, heart attacks, and strokes that require considerably more extensive medical intervention.

In the Notice, the IRS expands the definition of preventive care to include coverages for specific chronic illnesses, in order to encourage necessary care and mitigate the consequences of not receiving care. It is also pursuant to President Trump’s executive order released on June 24, 2019, which instructs the agencies to allow HSAs to cover other low-cost preventive care to help maintain health statuses of participants with chronic illnesses. Such conditions will be considered preventive care only if the care is for one of the conditions listed below, and only when the care occurs for the purpose of preventing exacerbation of the condition or development of a new, secondary condition. Any care, services, or conditions not listed within the Notice (or other IRS guidance) will not be treated as preventive care and will not be permitted under the preventive care safe harbor.

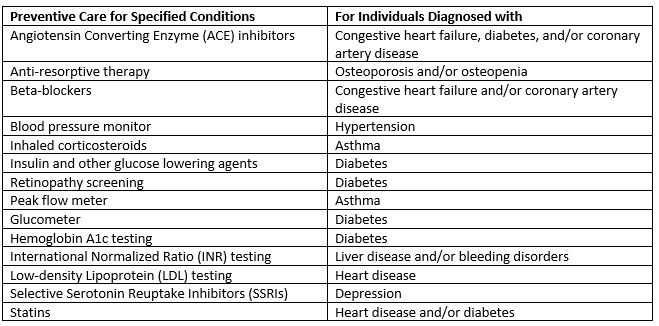

Preventive Care under Code Section 223 now includes the following care and conditions:

Impact on Employers and Plan Participants

Employers and plan sponsors that offer an HSA-qualified HDHP, and their participating employees, should understand which conditions and services are now included under the preventive care definition. While use of the expanded safe harbor is voluntary, we expect that many plans will adopt it. The expanded safe harbor could benefit employers—especially those with self-funded plans—and allow for further cost-savings by covering chronic illnesses before a deductible is met.

This message is a service to our clients and friends. It is designed only to give general information on the developments actually covered. It is not intended to be a comprehensive summary of recent developments in the law, treat exhaustively the subjects covered, provide legal advice, or render a legal opinion.

About the Author. This alert was prepared for Benefit Advisors Network by Stacy Barrow. Mr. Barrow is a nationally recognized expert on the Affordable Care Act. His firm, Marathas Barrow Weatherhead Lent LLP, is a premier employee benefits, executive compensation and employment law firm. He can be reached at sbarrow@marbarlaw.com.